The Competitive Landscape Of The 'Buy Now Pay Later' (BNPL) Industry

- pzconsultingbl

- Nov 21, 2022

- 2 min read

BNPL (Buy Now Pay Later) is a short-term financing both in store and online, allowing individuals to split their purchase into instalments and pay them later on. According to GlobalData, the industry has a global transaction value at USD 120 billion, and is forecasted to reach USD 576 billion in 2026.

Source: Statista

BNPL is becoming a huge trend in the financial services industry, with companies extending features in the payment options, increasing the tension among brands. Some of the these include:

July, 2021: Apple launch its ‘pay later’ feature, in partnership with Goldman Sachs to loan the instalments

Aug, 2021: Affirm partnered with Amazon in the US, whereby after the announcement soared Affirm’s share up to 46.67%

Aug, 2021: Square acquired Afterpay, the transaction was valued at USD 29 billion

Key players in the BNPL industry, in chronological order:

Klarna

Paypal

Affirm

Company | Company Profile | Number of Active Users | Number of Active Merchants | Audience Demographic / Main User Group |

Klarna | Founded in 2005 in Stockholm, Sweden | 150,000,000 | 450,000+ | 70% are Gen Z and Milllenials |

Afterpay | Founded in 2014 in Sydney, Australia | 20,000,000 | 144,000 | ~ 70% are Gen Z and Millenials |

Affirm | Founded in 2012 in San Francisco, US | 12,700,000 | 235,000 | ~ 50% are Gen Z and Millenials |

Why do consumers shift from traditional credit/debit cards to the BNPL system?

Due to the pandemic in 2019, lockdowns are implemented, people need to stay indoor, increasing online shopping demand

BNPL lets customers use the service free of charge, or without interest, under certain conditions (If they fail to pay back on time, additional charges are implemented). The process happen through just one click, which helps them avoid the hassle they will get at the bank

An appealing option for customers, as the service is offered on different product ranges (luxury, necessities)

Loyalty programs from the large BNPL brands give consumers incentives to keep using their service. (did you know, 69% of US consumers say loyalty programs influence their purchase decisions)

Klarna acquired Stocard to launch its digital loyalty card directly on their app, avoiding the hassle of plastic cards. You earn points with every purchase and collect your benefits and rewards at the merchants

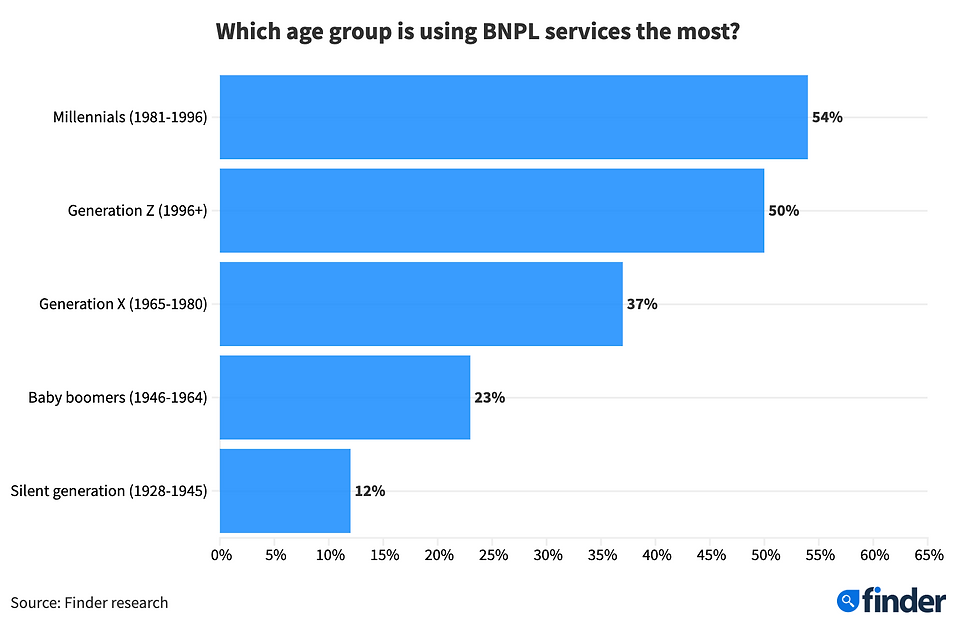

Who uses BNPL?

According to Bain&Company, there were 10.1 million BNPL users in the UK. The most popular age range to use this service are Gen Z and Millenials, but also is quite common among higher age range as well.

Comments